What separates a first-time fund manager who closes institutional capital from one who never gets a second meeting? Often, it’s not the strategy. It’s the data room.

Most emerging managers obsess over their pitch. The deck. The narrative. The 45-minute meeting. And then they win the meeting — and lose the process. Because when the serious LP sends over their due diligence checklist, what comes back is a Dropbox folder with four PDFs, two of which are the wrong version, one that’s password protected and one that has not been updated for 15 months.

This is not hypothetical. It happens every week.

The GP data room is your operational credibility made visible. It tells an LP three things before they’ve read a single page: whether you’re organized, whether you’re serious, and whether you’ve done this before. For first-time fund managers — where institutional trust doesn’t yet exist — the data room may be the single most consequential structure you’ll ever build.

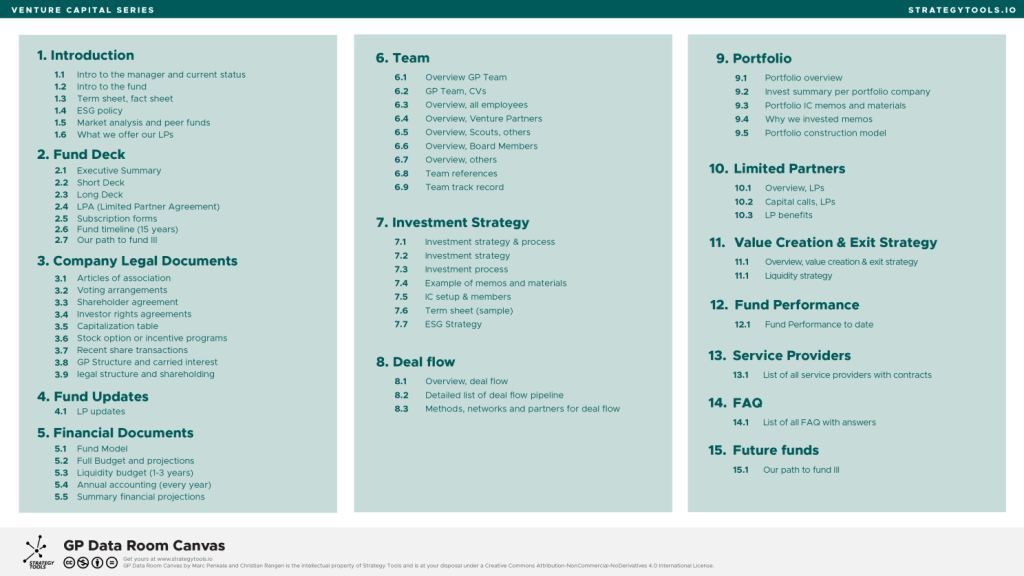

We’ve mapped the full architecture of a professional GP data room in the GP Data Room Canvas, covering 15 categories from Introduction to Future Funds. In this article, we walk through four real-world cases — the bad, the weak, the good, and the outstanding — to show exactly what passes institutional scrutiny and what doesn’t.

Why the Data Room Is a First-Time Fund Manager’s Credibility Infrastructure

When an established manager like a Sequoia or Benchmark raises a new fund, they don’t need a data room to establish trust. The brand does it. The track record does it. The relationships do it.

You don’t have that.

What you have is process. And the data room is the physical manifestation of your process. When an LP — a family office, a fund of funds, an institutional allocator — opens your data room, they are asking: Can this team execute? Are they organized? Do they think ahead? Can I trust them with $10 million of our capital over 12 years?

A bad data room doesn’t just slow down due diligence. It ends conversations.

Let’s look at the four cases.

Case 1: The Ugly — “Venture Capital Partners Fund I” (VCP)

A two-person team, former consultants, first-time fund, targeting €30M. Strong network. Compelling thesis. Disastrous data room.

VCP had been fundraising for 14 months. They had great coffee meetings. They got into diligence with seven LPs. They closed zero.

When we reviewed their data room, here is what we found — or rather, what we didn’t find.

Section 1 — Introduction: A single two-page PDF labeled “About Us.” No fact sheet. No term sheet. No ESG policy. No market analysis. The intro to the fund was three bullet points inside their pitch deck.

Section 2 — Fund Deck: A 22-slide deck, version 7, filename “FinalFINAL_v7_USE THIS ONE.pptx.” No LPA. No subscription forms. No fund timeline. When asked for the LPA, the team said, “We’re still working with our lawyer on that.”

Sections 3 & 5 — Legal and Financial: Empty. No articles of association for the GP entity. No cap table. No fund model. No budget. The team had a verbal financial model they could walk through on a call, but nothing documented.

Section 6 — Team: Two CVs in PDF format. No references. No track record documentation.

Section 9 — Portfolio: A list of eight companies they had “advised or angel invested in” informally, with no documentation of ownership, no investment memos, no IC process described.

The result: Every LP who opened this data room and got past the first folder understood immediately: this team is not ready. Not because their thesis was wrong. Not because the people were bad. But because they had no operational infrastructure. They couldn’t tell the story of how a decision gets made, how money moves, how LPs would be protected, or how the fund actually works.

The specific failures:

- No LPA at 14 months into fundraising

- No fund model or financial projections

- No formal track record documentation (item 6.9)

- No investment process documentation (7.3)

- No IC setup described (7.5)

- No GP legal structure (3.8, 3.9)

- No service provider list (13.1)

The lesson: A data room with missing legal and financial foundations doesn’t signal “early stage.” It signals “not serious.” An LP cannot write a check to a fund that cannot explain its own legal structure.

Case 2: The Bad — “Nordic Deep Tech I” (NDT)

Three partners, one with prior VC experience, targeting €50M, deep tech focus. Professionally run. Data room built in a rush.

NDT had raised €15M from friends and family. They were now pitching institutional LPs — fund of funds, development finance institutions, one family office. They had a data room. It was just… wrong in the ways that matter most to institutions.

Section 1 — Introduction: Solid intro to the team. Clean fact sheet. No ESG policy. When pushed on it, the team said, “ESG is embedded in our thesis.” This is the wrong answer. Every institutional LP has an ESG checklist. A verbal commitment is not documentation.

Section 2 — Fund Deck: Good short deck. No long deck. No LPA — they had a term sheet for the fund, but the actual LP Agreement was “being finalized.”

Section 3 — Legal: Articles of association existed. No capitalization table for the GP entity. This matters because institutional LPs want to understand carried interest economics and GP incentive alignment before they commit. Who owns what? What happens if a partner leaves?

Section 5 — Financial: Fund model existed — a good one, actually. But the liquidity budget (5.3) was missing, and the annual accounting (5.4) showed only Year 1. LPs running 10-year models need to see the full 15-year fund lifecycle, at minimum in projection form.

Section 7 — Investment Strategy: Investment strategy was well documented. But there were no example memos or materials (7.4). For first-time managers, this is critical. LPs can’t assess your judgment based on a strategy document alone. They need to see a real or illustrative investment memo — how you think, how you structure an argument, what diligence looks like in practice.

Section 8 — Deal Flow: NDT had impressive deal flow — 200+ companies reviewed in 18 months. But it was not documented. No pipeline list. No sourcing breakdown. Just a verbal claim on a slide. An institutional LP will ask: how do you know you’re seeing the best deals? Where does your deal flow come from? If the answer is “we’re well connected,” that doesn’t survive diligence.

Section 12 — Fund Performance: Listed DPI of 0, TVPI of 1.1x on their informal angel portfolio. But the methodology wasn’t explained, the valuations weren’t audited, and the comparison wasn’t made to a benchmark. Presenting unaudited performance numbers without context is worse than presenting no numbers — it raises questions.

The result: NDT got to final stages with three LPs and closed none on the institutional side. They eventually closed the fund off high-net-worth individuals, at a smaller size than targeted. Two of the three institutional LPs gave the same feedback: “Not ready for institutional capital. Come back with Fund II.”

The specific failures:

- No ESG policy document (1.4, 7.7)

- LPA not available during diligence (2.4)

- No GP cap table (3.5)

- No GP carried interest structure documented (3.8)

- No example IC memos (7.4)

- No documented deal flow pipeline (8.2)

- Unaudited, uncontextualized performance data (12.1)

The lesson: A data room that has most of the pieces but is missing the institutional-grade items — LPA, ESG, memos, documented deal flow — will fail with institutional LPs even if the team and thesis are strong. Institutional allocators are not trying to be difficult. They have compliance obligations, investment committee requirements, and fiduciary duties. They cannot make exceptions.

Case 3: The Good — “Meridian Ventures Fund I” (MVF)

Solo GP with a strong operator background, targeting $40M, B2B SaaS focus, US market.

Meridian had one thing working against them: a solo GP setup, which many institutional LPs won’t back. But their data room was so comprehensively built that it answered every objection before it was asked.

Section 1 — Introduction: A three-page fund introduction that included current fundraising status (amounts committed, amounts soft-circled), a clean two-page fact sheet, a one-page ESG integration policy, a market analysis benchmarking the fund against 12 comparable B2B SaaS early-stage funds, and a clear articulation of LP benefits — co-investment rights, quarterly reporting, annual LP meeting.

Section 2 — Fund Deck: Executive summary (two pages), a 15-slide short deck, a 40-slide long deck, a fully negotiated LPA reviewed by a top-tier fund counsel, subscription forms ready to execute, a 15-year fund timeline with capital deployment milestones, and a clear narrative of the path to Fund II.

Section 3 — Legal: Complete. Articles of association for the GP entity, voting arrangements, shareholder agreement for the management company, investor rights agreements, clean cap table (the GP was co-owned 70/30 by the solo GP and a venture partner), stock option plan for future team hires, and full GP structure documentation including carried interest mechanics.

Section 5 — Financial: A bottom-up fund model with scenario analysis (base, bull, bear), a full 15-year budget with management fee projections, a full 15-year liquidity budget, and summary financial projections in one-page form.

Section 6 — Team: Comprehensive. Full CVs, references (three per team member), and — critically — a documented track record section that included every angel investment the GP had made, with ownership percentages, invested amounts, current valuations, and methodology.

Section 7 — Investment Strategy: Full investment strategy document, a separate investment process flowchart showing stages from sourcing to IC to term sheet to close, three example investment memos from actual investments (redacted), IC structure, a fund-level sample term sheet, and a standalone ESG document.

Section 8 — Deal Flow: A pipeline dashboard showing 340 companies reviewed over 24 months, broken down by source (network introductions 45%, inbound 30%, proactive outreach 25%), stage, and sector. A documented list of 20 top-priority pipeline companies with status.

Section 9 — Portfolio: Five investments documented with full IC memos, “why we invested” write-ups, portfolio construction logic, and a portfolio model showing expected follow-on reserves, ownership targets, and exit scenarios, broken down per company, per year. Importantly, there was a clear logic linking the investment strategy, term sheet and portfolio construction.

The result: Meridian closed their $40M fund in nine months, with three institutional LPs including a fund of funds. The solo GP structure was challenged, but the depth of documentation — especially the track record documentation, the example memos, and the clear GP legal structure — converted skeptics into LPs.

What made it work:

- Complete legal documentation from day one

- Track record presented with methodology and transparency

- Example investment memos showing actual decision quality

- Deal flow data quantified and sourced

- LP benefits articulated clearly (10.3)

- Path to Fund II described concretely (15.1)

Case 4: The Outstanding — “Ember Capital Fund I” (ECF)

Two GPs, one former operator (Series B exit), one former institutional VC (eight years at a top-tier fund), targeting CAD$75M, climate tech.

Ember built their data room the way great operators build products: with the user — the LP — at the center. Before they launched their data room, they interviewed 55 institutional LPs and eight fund of funds to understand exactly what was missing in the emerging manager data rooms they reviewed most often.

Then they built to that spec.

Sections 1-2 — Introduction and Fund Deck: Standard excellent execution. But they added one thing nobody else does: a live fund dashboard accessible through the data room, showing real-time fundraising status, committed capital, and timeline. LPs who had soft-circled could log in and see the momentum. This is psychological — it creates conviction and urgency simultaneously.

Section 3 — Legal: Not just complete, but annotated. The LPA came with a two-page plain-English summary of key terms — management fee, carried interest, clawback provisions, LP removal rights, key person clause. Most LPs are not fund lawyers. The team who explains their own legal documents is the team that earns trust.

Section 5 — Financial: The fund model was scenario-based and interactive (an Excel model, not a locked PDF). LPs could adjust deployment pace, loss ratio, and exit multiple assumptions and see outputs in real time. Footnotes explained every assumption. This is remarkable for a first-time fund.

Section 6 — Team: Beyond CVs and references, Ember included a “team working agreement” — how decisions get made between the two GPs, what happens in disagreement, the succession plan if a GP leaves. This document doesn’t exist in 99% of first-time fund data rooms. It answers the most common unasked question in every LP’s mind: What happens if these two people have a falling out?

Section 7 — Investment Strategy: Five full investment memos from actual investments. A documented IC process that included a devil’s advocate requirement — one partner formally argues against every investment before a decision is made. An ESG strategy that wasn’t a policy statement but a 12-page integration document showing how climate impact was scored alongside financial returns.

Section 8 — Deal Flow: A deal flow database showing 18 months of activity, 420 companies reviewed, sourcing channels, conversion rates at each stage, and a network map of their top 30 deal flow partners. They had exclusivity or right-of-first-refusal agreements with three university deeptech transfer programs documented in the data room.

Section 10 — Limited Partners: LP overview with anonymized profiles of all committed LPs showing type, geography, and ticket size. Capital call mechanics explained with sample notices. A full articulation of LP benefits including co-investment policy, information rights, and annual meeting format. Clear articulation of LP value proposition for different categories of LPs.

Section 11 — Value Creation and Exit Strategy: A 10-page value creation playbook describing exactly how Ember works with portfolio companies post-investment, with documented frameworks and case studies from the partners’ prior experience. Exit strategy documented by sector, showing comparable transactions and target ownership thresholds.

Section 12 — Performance: Full documentation of both partners’ prior investing track records, with verification methodology, auditor letter, benchmark comparison (Cambridge Associates vintage year), and attribution analysis showing individual partner contribution.

Section 14 — DDFAQ: 104 FAQs with thorough answers. Built from actual LP questions received over 18 months. This alone saved dozens of hours of back-and-forth email chains with LPs in diligence.

The result: Ember oversubscribed their CAD$75M fund at CAD$88M in seven months. They received interest from LPs they had never contacted — word spread through the LP community that the data room was the best they had seen from a first-time manager. One fund of funds LP told them directly: “We’ve backed 40 emerging managers. Your data room was in the top three we’ve ever seen. That told us everything we needed to know about how you’ll run the fund.”

The Pattern: What Actually Passes Institutional Scrutiny

Looking across these four cases, the gap between good and bad is not talent. It’s preparation and intentionality. Here’s what consistently separates emerging managers who close institutional capital from those who don’t.

The six non-negotiables for institutional diligence:

1. A finalized LPA, available from day one. Not “being drafted.” Not “almost ready.” LPs cannot commit to a fund without reviewing the LP Agreement. If your LPA isn’t ready, you’re not ready to run a diligence process. Sure, you can wait for an anchor to set the terms for you, but is that really what you want…?

2. A documented track record with methodology. Every angel investment. Every board seat. Every advisory role where you had information rights. Presented with invested capital, current value, methodology for valuation, and attribution. An unaudited claim is not a track record. A documented, explained, attributed record is.

3. At least two real investment memos. Strategy documents show intent. Investment memos show judgment. LPs back people, and people are revealed in the way they make decisions. An IC memo — even redacted — is one of the most powerful documents in your data room.

4. A documented investment process. From sourcing to IC to term sheet to close. Who votes. What constitutes a veto. How long it takes. What the post-investment monitoring looks like. Process is proof of professionalism.

5. Clear logic from investment strategy to term sheet and portfolio construction If the deck says “can invest opportunistically at pre-seed” or “will follow-on with the winners”, make sure this is actually reflected in the portfolio construction tab in the fund model. If, “will exit selected deals at series A” is a pillar of your liquidity strategy, make sure you have this right embedded in your term sheet.

6. A complete GP legal structure. Who owns the management company. How carried interest is split. What happens if a GP exits. Key person clause triggers. LP removal rights. These are not details — they are the foundation of the trust relationship between you and your LPs.

Building Your Data Room: A Practical Approach

The GP Data Room Canvas organizes this work across 15 sections, from Introduction through Future Funds. For first-time managers, we recommend building in three phases:

Phase 1 — Foundation (before first LP meeting): Sections 1, 2, 3, 5, and 6. Introduction, Fund Deck, Legal, Financial, and Team. These are the table stakes. If these are incomplete, you have no business having an institutional LP conversation.

Phase 2 — Differentiation (before diligence kicks off): Sections 7, 8, 9, and 12. Investment Strategy including example memos, Deal Flow documentation, Portfolio overview if you have investments, and any Performance documentation. This is where you separate yourself from the crowd.

Phase 3 — Excellence (ongoing, refined through diligence): Sections 10, 11, 13, 14, and 15. LP documentation, Value Creation strategy, Service Providers, FAQ, and Future Fund path. Build the FAQ in real time as LPs ask questions. Update the service provider list as you appoint advisors. These sections are the mark of a manager who is building for the long term.

The Real Benchmark

The question is not: Does my data room have everything?

The question is: Does my data room answer every question an institutional LP will have before they ask it?

The best emerging managers treat the data room not as a checklist to complete, but as a product to design. They think about the LP experience. They think about the LPs journey through the data room. They think about the questions behind the questions. They think about what they would want to see if they were on the other side of the table.

Ember Capital built a data room that circulated through the LP community organically. Nordic Deep Tech spent 18 months fundraising and came away with nothing from institutional LPs.

Same market. Same asset class. Same fund size target.

The data room is never just a folder of documents. It is the first proof point of how you will run your fund.

Build it accordingly.

The GP Data Room Canvas is a free tool from Strategy Tools, designed to help emerging managers build institutional-grade fundraising infrastructure. Download it at strategytools.io.

Want to assess your own data room? Use the Canvas as a checklist: 15 sections, 60+ line items. Any section that is incomplete or undocumented is a potential reason an LP doesn’t write you a check.