The nine cap table mistakes founders make in Scale Up!

Christian Rangen

Strategic advisor to CEOs, Boards, governments, innovation agencies, startup- and venture ecosystems, Fund-of-funds & innovation clusters. Run global GP accelerators. Author, Speaker, Faculty. Chair, Link Capital

April 23, 2026

The Scale Up! programs are built on 20 years of hard earned experience investing, building, scaling and exiting tech companies. One thing that can kill deals: bad cap tables, something every accelerator can advice and mentor founders on.

In Scale Up! we give founders years of cap training confidence in mere days. Across 7.000 participants, here are the nine most common mistakes founders make in Scale Up!

Most accelerator programs focus on the first steps of the journey. First customers. Early revenue. Product MVP. First two hires. AI stack. Impact philosophy. Pitch deck. Demo day. Closing the next SAFE round. All good, important things.

Yet, in our work with accelerators and startup programs around the world, we often see a vast gap around growth strategy, scaling up, capital strategy and entreprenurial finance readiness. One key topic that stands out: cap table management, or more specifically, how to correctly manage your cap table from idea to successful exit, and make sure you can structure and negotiate on this across your future funding rounds. Most founders, leaving lot of room to improve.

Here are the nine most common cap tables challenges we see for founders on the journey from idea to liquidity.

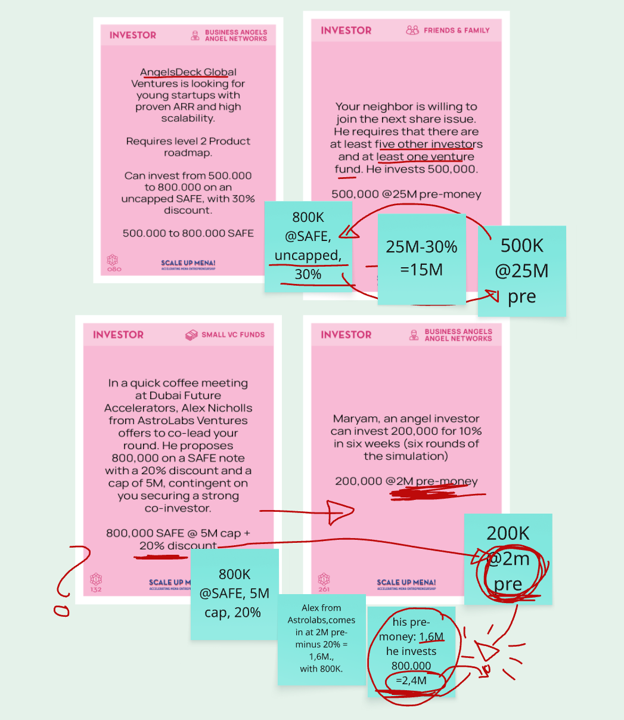

1. Stacking SAFEs and SAFE conversions

Want to step into a minefield of cap table complexity? Look no further than stacked SAFEs and (attempts at) SAFE conversions. In our experience, 90% get this wrong – and most come back to us and share “this is exactly what we are struggling with in real life too”.

Imagine a team, five founders. They raise $100.000 uncapped, 20% discount from a brother. Four weeks later they raise $50.000, 2M cap from an uncle. Things are working. Two months later, they take on $180.000 from 4 angel investors, each with $20.000 – $80.000 1,5M cap, with 25% discount and MFN. They accelerate. Join an accelerator program. Accelerator offers standard terms, $150.000, at a $1,25M post cap.

Six weeks after demo day, Local VC comes in, offering $250.000 at a 2M pre-money valuation, with 20% ESOP pre-round, six years reverse vesting, requiring all SAFEs to convert into common shares.

Now, without realizing, they are sitting on this beautiful phenomenon called ‘stacked SAFEs’, where the startup has taken in four different SAFE notes, each with somewhat different terms. Looks easy on paper. I mean, how hard can it be?, right? Well, turns out few can actually structure and convert that correctly, slowly realizing that “honest mistakes were made” in the early days; blaming “we are all doing this for the first time”.

2. ESOP, ESOP Management

You would think it would be easier, but setting up and managing an Employee Stock Option Program is something few get right.

From initial setup, “how much should we allocate?”, the difference between “allocated and distributed”, and “disbursement for key personnel along the way”, most teams fumble here. By the time we get to an exit transaction, ESOP management is a mess with few able to account for how key people shares were given, distributed and then lost again.

3. Foundational equity, vesting and leavers

One of the key pillars of a full Scale Up! Program is Foundational equity. Often, when people ask “can we run Scale Up! in 1 day, our founders don’t have time for more”, I ask “how many of your founders have a fully prepared foundational equity agreement in place, legally valid, signed by all stakeholders and sitting inside your accelerator’s portfolio company folder?” Accelerator leaders stop flat. Most don’t know what I’m asking them.

But I am asking them the questions, which might save their entire investment four years down the road, when the four person founders team split up, two break out to start something new, and the accelerator’s investment manager slowly realizing there is no clause or terms on how to deal with this, ultimately letting the two breakout founders walk away with their 14% equity each, making the company uninvestable, slowing spinning into a complete write-off.

Surprisingly few founders – and accelerator managers – understand foundational equity. How initial equity is split, set up, dealing with advisory shares (ASOP), Board shares (BSOP), leaving mechanisms, vesting schemes, common vs. preferred and more. The reading is 60 pages. But it is golden.

We practice this in the program. We build deep skills by doing, not listening. We have founders study this in their reading materials. But most importantly, we save the accelerator’s investment before they even knew it was needed.

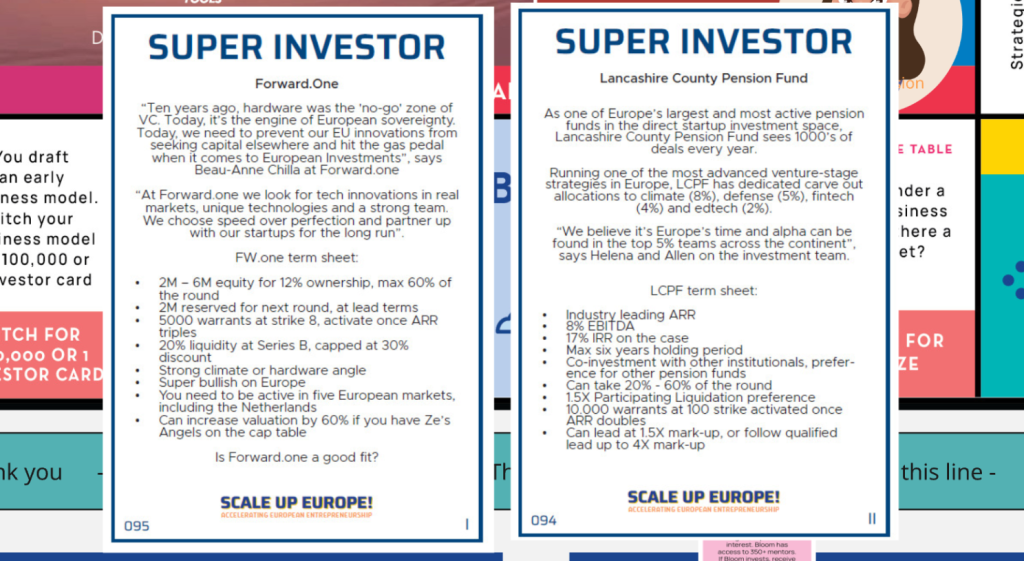

4. From term sheet to investment

“So, we got an offer…..”, so often begins the discussion leading to the inevitable key milestone; first priced round.

We are now, often, in day two. Teams have been working hard. Many are sitting on a series of stacked SAFEs. They have been working to raise a price round. Maybe a late seed. Maybe a Series A.

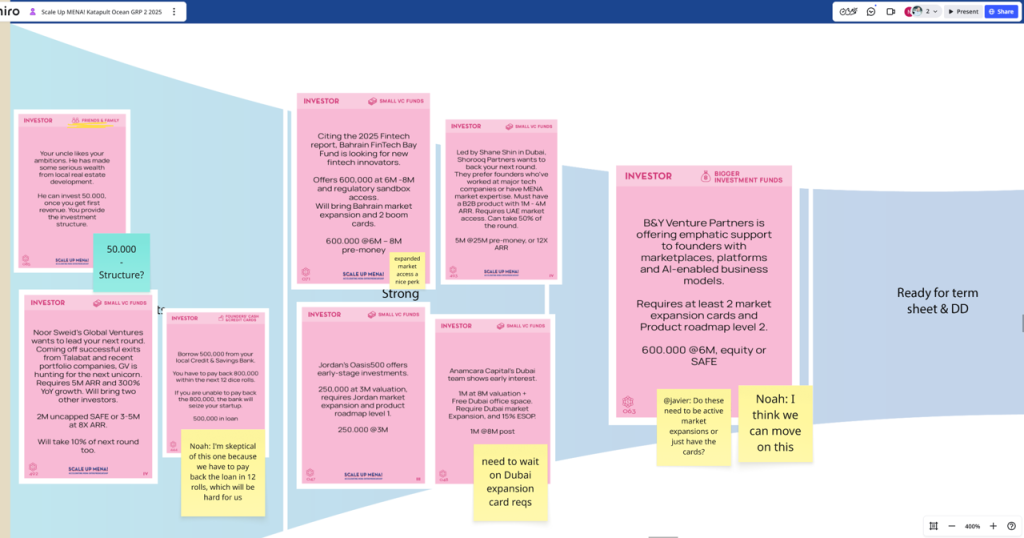

They got the term sheets, in Scale Up! these are the investor cards. They’ve spent time to develop a long-term funding strategy, a capital strategy, planning out their Series A, B, C, D, ideally with a 3x valuation mark-up and sub 20% dilution. “But how do we plug this into the spreadsheet?”, founders commonly ask. But the question is more precisely, “what are the implications on our cap table now that we have said yes, decided to do it, and don’t understand quite what we just said yes to?” Term sheet (example)

Golden Gate Ventures offers to lead your Series A, taking 50% of the round, capped at 2,4X last post, or 8X forward ARR. Requires a 20% ESOP top-up, reserved 3 % advisory shares, 1x standard liquidation preference and full anti-dilution provisions.

“How do we put that into our cap table?”

What I always ask, “can you explain what you just said yes to, what you have decided to do here? Few can. I wish that was not the case.

5. Closing a syndicated round

“Hey, Chris, we have six investors that want to come in. What do we do?”, or even better “We got six investors, we got the money, but we did not put them into the cap table yet….” A syndicated round is an investment round with two or more investors, all coming in on the same terms.

“We raise 12M, from these six investors. What do we do now?” Just like the point above, the question is always, ‘what’s the impact on our cap table and how do we keep track of it?’

Working through examples, we show how to structure a syndication, how to split up the round and bring each investor onto the cap table, and how to track all preference terms. Sometimes, we test the founders’ knowledge and confidence in doing this IRL. It leaves much to be improved.

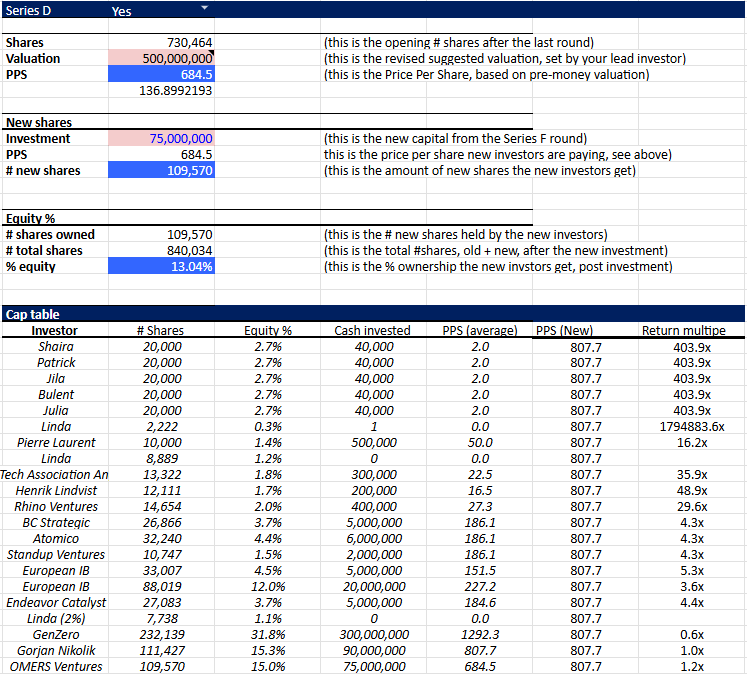

6. Warrants and options

“It says, ‘series A lead as 20.000 options at 8 strike, to be implemented once ARR hits 20M. What does that mean?” Well, in the eagerness to close out the series A, founders took on terms….. they they did not understand, with implications they can never roll back. In this case, let’s say that the Series A price per share was 550, and a fully diluted cap table was 150.000 shares. Now, suddenly, with ARR velocity through the roof, the company suddenly has it’s Series A lead, calling an option to purchase another 20.000 shares at only 8 per share. That’s a 98,5% discount, for a 13,3% equity piece, that no founder actually understood when they signed. Ooops.

Well, we would rather this happens in the Scale Up! program rather than real life. Still happens in real life, though.

7. 2X liquidation preference, participating

“Chris, we took this term sheet with a 2X liquidity or something. Is that good?”.

Fortunately, most founders around the world are growing familiar with liquidity terms and liquidity stacks. Yet, surprisingly, few can actually map this out on a whiteboard correctly.

In this case, seeing any liquidation preference might lead founders into a tailspin. What is it? It must be bad? How do we count it? (well, it says 2x). We don’t like it. But, honestly, we don’t really understand it. In our experience, liquidation preferences only rarely come into effect; but when they do, the impact can be devasting. An angel with a liquidation preference is quite harmless, as well as quite rare. A Series C, $60M with 4X liquidation preference on the other hand, can be a nuclear bomb.

I believe it is absolutely critical for founders to understand liquidation preferences, why they exits, why (some) investors have them, how they might come into effect (but often do not), what the math maths out to, and what the impact on the cap table might be. Key word: might be.

But, better to learn this in Scale Up!, rather than learning the hard way; in real life.

8. Partial secondaries

“It says, bpiFrance wants to lead series C, capped at 65% of the round once two other banks are ready to join; requires to buy out 50% of pre-seed and seed investors, at a 25% discount….”

In real life, startups’ ability to generate investor liquidity is crucial. It is the lifeblood of the ecosystems ability to grow and expand over time. No liquidity. No life. No liquidity. No new investments happening. The ecosystem dries up. For many accelerators, liquidity is an afterthought in the excitement of launching a new cohort, but an existential challenge a decade later when DPI becomes the cause behind your ulcer.

What we see, across the board, is that less than 10% of the participants in Scale Up! can correctly complete and update a partial secondaries transaction like this. If they can’t do this in a ‘supportive’ Masterclass environment; how are they possibly going to be able to handle this in a late-seed negotiation in real life?

More importantly, how are accelerators equipping them to navigate term sheet negotiations on this, we wonder?

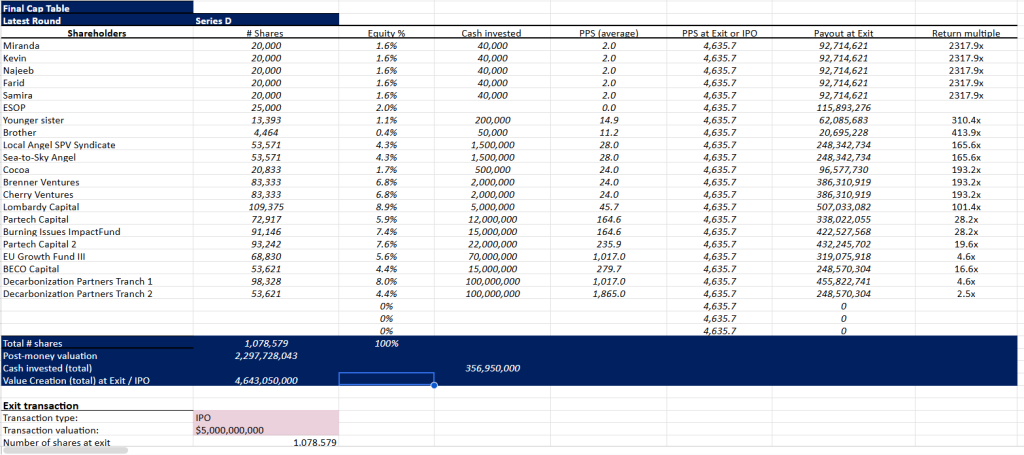

9. Exit transaction

“Chris, how do we exit….?” The million-dollar question asked by 99% of the participants.

At the end of every (successful) founder’s journey, there is likely to be an exit transaction. (note, we run a series of Accelerator plug in programs only on ‘exits & liquidity’. A lot of misunderstanding here, with the term ‘exit’ being wildly misunderstood. After a 3-hour sessions, 90% go, ‘ah, oh, ok, now I understand’) Maybe not a full exit transaction with founders leaving, but at least a liquidity event for investors. Same goes in the Scale Up! Masterclass. We usually run into an exit transaction. This, unfortunately, is where a lot of founders really stumble.

- Understanding deal terms: weak

- Understanding implications of the liquidation stack: weak, or even entirely forgotten

- Understanding how to manage the exit transaction in the cap table: weak

- Actually grasping the full financial journey, for founders, team and investors alike: pretty weak

How, I often wonder, are these founders going to be able to convince, lock in and bring on board investors, most of whom are themselves measured on DPI and distributions, when the founders are barely able to manage an exit transaction served on a card and a golden platter?

How can we ensure that more founders, fully appreciate the ‘exit at the end of the journey’, and use that narrative in their early-stage fundraising pitches?

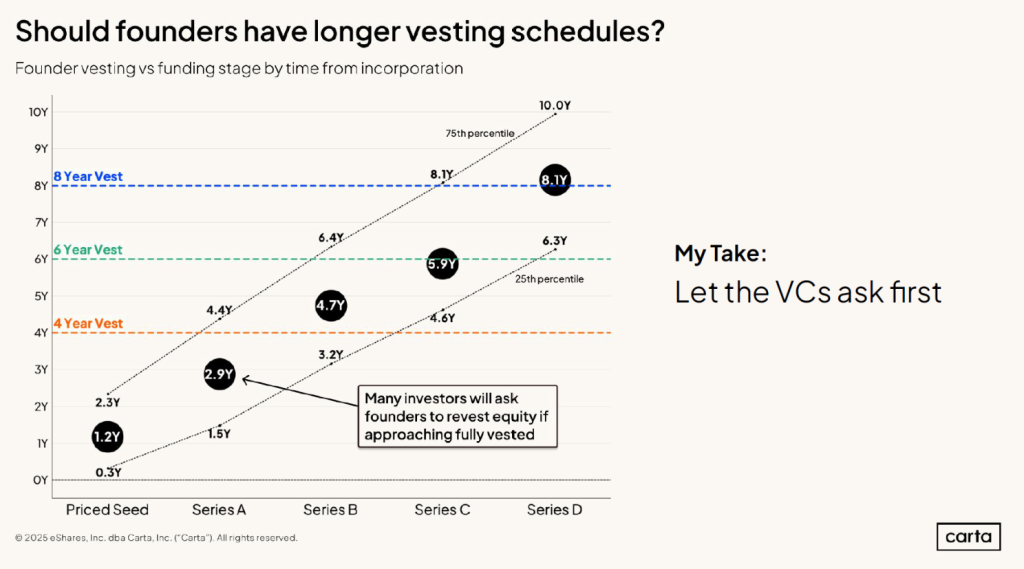

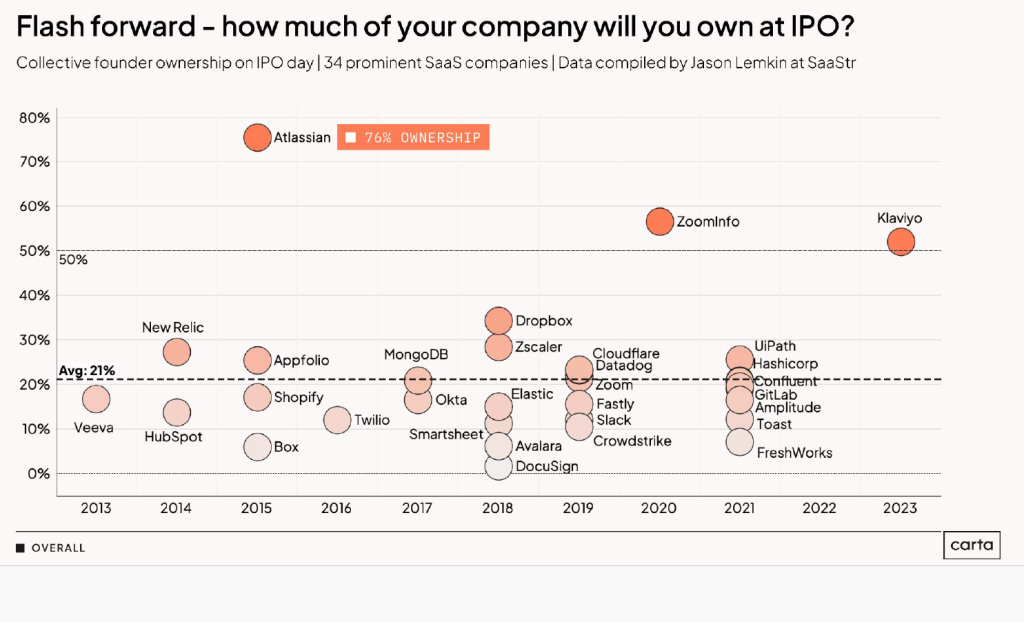

Bonus: how much do you target to own at IPO?

To many founders, the question seems preposterous. IPO, if ever, must be years away, they say. That might be true, but the path and preference terms get set now and in the next round(s) you close.

I show this slide, from Carta. Most people are shocked when they see founders owning 2% – 10% at IPO.

For accelerators, how are you preparing your founders for the right capital strategy to strike the right cap table outcome?

Why 7.000+ founders, angels and investors love Scale Up!

In Scale Up! we don’t teach entrepreneurial finance. We give founders mastery. We train people to read term sheets and negotiate in real-time on the terms that truly matter.

“Chris, you have no idea how much the Scale Up! program helped me when we closed our recent round. For the first time, we actually understood what some of the investors were talking about and we could negotiate with them head on. Thank you”, said a female founder in Cairo, Egypt after closing her seed round led by international investors.

Cap table mastery. Sharp term sheet analysis. Founder-investor negotiation confidence. All outcomes from the Scale Up! Programs. All available to you and your accelerator cohort.

Accelerator manager, innovation agency, ecosystem developer? Want to bring Scale Up! Programs into your ecosystem? Let’s talk!

Scale Up! fast facts:

- 7.000+ people completed to date

- Equips founders for the full journey from idea to exit

- Used widely across accelerators, incubators, angel networks, ecosystem development, innovation agencies, entrepreneurship organizations globally