The New Nordics has the potential to become one of the world’s leading, most recognized, high-output, value creating ecosystems. Here are two tools, based on our global experience developing startup ecosystems, venture capital ecosystems and innovation clusters that can push the New Nordics forward.

By: Christian Rangen, advisor, faculty, investor

We have invested in founders in Estonia. Helped VC funds in Finland raise LP Capital in Norway. Sat on boards with Swedish board members. Raised follow-on rounds in Danish startups, developed innovation clusters in Finland; advised innovation agencies in Norway; yet, we have never, seriously, studied the Nordic- and Baltic ecosystem as one. Until now.

In late 2025 we started reading up ‘the New Nordics’ (thanks, byFounders). Increasingly, it dawned us on that the New Nordics has every possibility to emerge, to step up, to take its place as a top 5% global ecosystem.

Today, Sweden is known for its AI successes, its savings culture, it’s IPO market. Denmark is known for its life sciences and tech talent, its ecosystem events and energy leadership. Estonia for its deep tech founders, e-government and it’s incredible VC investments measured in % of GDP (most recent data 3,2% of GDP vs. a global aspiration to hit 1%). Yet, we are not even remotely maximizing the value, the potential, the upside of our shared, collective, New Nordics ecosystem. We are, if you will, choosing to stay a league or two below our potential.

Over the past 15 years, I’ve had the opportunity to work on ecosystem-, cluster- and scale up initiatives in more than 65 countries. From Canada to Fiji, from South Africa to Sweden, from United Arab Emirates to United Kingdom, as well as teaching best practices in venture capital and entrepreneurial finance in places like Lausanne and London.

Yet, a single, united ecosystem perspective for the New Nordics was never on the radar. That started changing in late 2025.

Slowly, it emerged, a pattern, where ‘clearly, we needed to connect the dots’. From a rising need for connecting our defense startup ecosystem initiatives (see, Final Frontier, DIANA, Nato Innovation Fund and Nordic Defence Innovation Foundry and TheFactory DefSec Accelerator), to multiple ecosystem initiatives (see, Nordic Deeptech Valley, Sweden’s excellence clusters, Nordic Innovation Houses), to a number of GP/LP capital initiatives (see, TechBBQ LP Forum, Nordic GP/LP Summit, Arctic15 LP Summit, Finland’s Venture Nordics Program and Nordic Growth & Capital Attraction), to a need for more and more well-connected liquidity paths across the region (see, Nordic Secondaries Fund, Siena Secondaries, Nasdaq First North Growth Market in Stockholm and a deep bench of PE firms).

Across the board, we started seeing ‘a lot of pieces’, but still much work remaining to develop the shared platforms, dense networks and strong ‘connective tissue’ across the region.

Based on our work with innovation clusters (Building Innovation Superclusters, 2019, National Cluster Programs, 2021), startup ecosystems(2020, 2020) and venture capital ecosystems, (2023, 2026), and developing visual ecosystem development tools for programs in places like Malaysia, Canada, Costa Rica and Saudi Arabia; we’ve been exploring the new landscape of the New Nordics, trying to assess what the right building blocks might be, identify the gaps to be solved and structure a visual language that can enable us, jointly, to develop a new framework for ecosystem development in the New Nordics.

Part of the most recent inspiration comes from the ongoing Nordic Innovation Ecosystem Mobilization project, already doing excellent and vitally important work in this space. I’ve used some of their category language, to align how we speak about the same building blocks. I’ve also suggested several key building blocks, based on our experience, that are vital to any healthy, thriving ecosystem.

We have then brought this together in the New Nordics Ecosystem Scaling Canvas.

See also The Tale of Two Ecosystems – and why it matters here

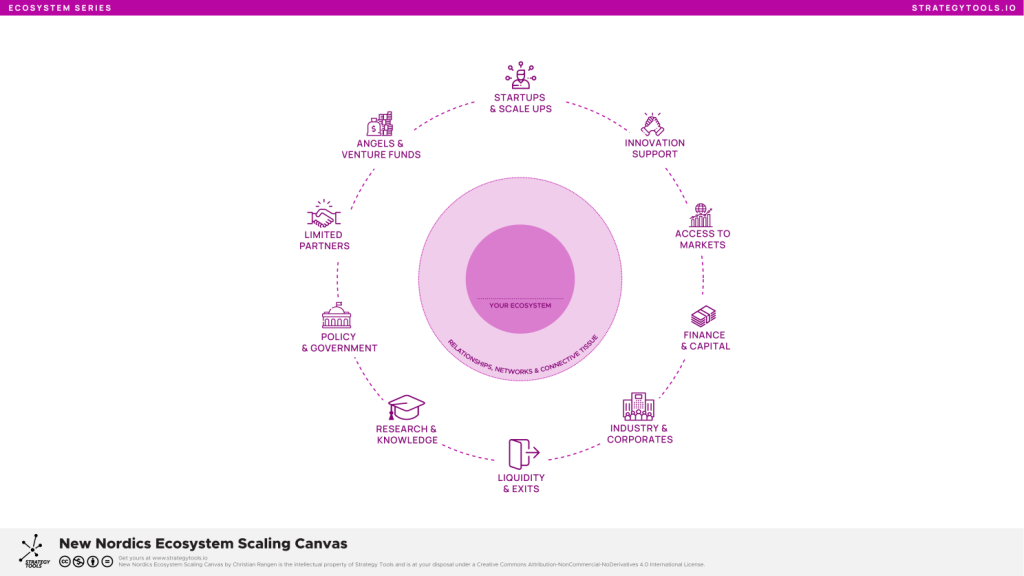

The New Nordics Ecosystem Scaling Canvas

Based on our work with global ecosystems and developing powerful visual tools for well over a decade, we brought ten key building blocks into the canvas.

This 10-part, or Decuple Helix, canvas then serves as a backbone for multiple visual canvases to support and develop the ecosystem across the New Nordics.

Startups & scale-ups are the engine of the whole system. Mapping them means counting not just seed-stage activity but the density of companies crossing €10M, €25M, and €100M revenue thresholds — the real test of whether a region scales, not merely starts. We are counting Colts and looking for Thoroughbreds, maybe more so than we chase inflated unicorns.

Innovation support covers accelerators, incubators, co-working spaces, and hubs. What’s the infrastructure we need to grow and scale? The honest way to assess this block is by founder outcomes rather than program input: how many alumni raise significant follow-on rounds, hire internationally, triple revenue YoY or reach Series A within three years? Across the region, we have a significant amount of innovation support; but is it optimized? Does it deliver the outputs we seek?

Access to markets is the Nordic Achilles’ heel. Small home markets force early internationalization, so developing this block means investing in soft-landing programs, export networks, and warm customer introductions into the US, DACH, and Asia. Equally, we need both government, public sector and private sector to become fast customers of startups; more important than any grant scheme is.

Finance & capital spans pre-seed funding, from grants, loans, early SAFEs, CNs and SLIPS through to growth equity. The candid assessment: Nordic seed is healthy, but Series B and beyond remains thin. Scaling here means attracting international growth funds and unlocking domestic pension and insurance capital currently sitting on the sidelines. We recommend using the Startup Investor Stack, and develop robust capital strategies from idea to IPO; not just solving with more grant financing. We need to be funding the entire journey, not just the first two steps.

Industry & corporates bring distribution, pilots, buying budgets, and acquisition appetite. Maturity in this block is measured by corporate-startup partnerships that actually close commercial deals and M&A exits, not by the number of signed MOUs or pilot programs completed.

Missing the big tech companies, e.g, like the US; we need more traditional industry, finance, manufacturing, life sciences, energy and defense to step up to the plate and be active customers of young companies. Having built companies here for 15+ years, we still have a long way to go together.

Liquidity & exits determine whether capital recycles. A region without active M&A and IPO flow starves its next generation of successfully exited founders, new fund managers and business angels. Developing this block means cultivating relationships with acquirers, building out thriving secondaries solutions and expanding Nordic exchanges as credible venues for tech listings. In our experience, it also means training founders, boards and management teams in liquidity strategies for early-stage and growth stage companies. Using the Entrepreneurial Finance Readiness Level (EFRL), our experience is that 90%+ of Nordic founders are not, fully, investor ready. This needs to change, and it can change at the ecosystem level.

Research & knowledge converts science into ventures. Map university spinout rates, tech-transfer terms, and PhD-to-founder pipelines — then benchmark honestly against Cambridge, ETH, and MIT to see where the gaps in commercialization really lie.

The region is strong in this space; world-class research; but miles to go to match that with the commercialization gene, ability to raise capital, bring research to market and scale companies around it.

Policy & government set the rules of play. The assessment question is simple: can a founder incorporate, hire globally, issue meaningful stock options, attract foreign investors, and exit without friction? Wherever the answer is no, that is the development agenda.

Do we have stable, entrepreneurship friendly governments? Yes. Can we do a lot better to compete for a top 5% global position? Yes, absolutely.

Limited partners are the invisible backbone. Without committed LPs — pension funds, family offices, sovereign wealth, endowments, CVCs, national fund-of-funds and the EIF— there are no emerging GPs and no venture funds.

Scaling this block means four things. First, broadening the LP base beyond the handful of public co-investors the region currently relies on. Second, accelerate pension reform to allocate into venture capital. Third, engage and develop a broad base of LPs across the LP Stack and finally, educate, train and upskill LPs across the New Nordics ecosystem. Teaching Venture Asset Management at IMD, now on its 3rd year, we hear from pension fund professionals and board members every semester, all describing the challenges they face bringing venture assets into the investment strategy.

We have a long way to go before our LP infrastructure is where it deserves.

Angels & venture funds are often misunderstood in ecosystem development. Mostly viewed as just sources of funding, we recommend thinking about the emerging fund managers, also as entrepreneurs. But rather than building a startup, they are starting an investment firm. Many emerging GPs say this is 4x as hard as building a startup.

Across the New Nordics, we need to ask ourselves, how do we develop a vast number of new investment firms, new VC funds and new angel networks; especially operator-led angel syndicates and specialist Series A/B funds with the conviction to lead rounds rather than follow. Emerging fund managers and emerging angel investors are just as critical across the New Nordics as startup founders are, and we need to scale them too.

Connective tissue; at the center sits what the canvas calls relationships, networks, and connective tissue — the informal layer that makes the other ten actually function. No building block works in isolation; a world-class LP base without exits dries up, and brilliant research without angels never get to market. Used together, the canvas becomes a practical instrument: a diagnostic for ecosystem builders, a planning tool for policymakers, and a shared language the New Nordics can use to move from promising to genuinely world-class.

From insights to strategy

Ok, so you’ve read the first part, a core construct of how to think more holistically about the New Nordics ecosystem. But what’s next? How to shift the conversation from understanding to action?

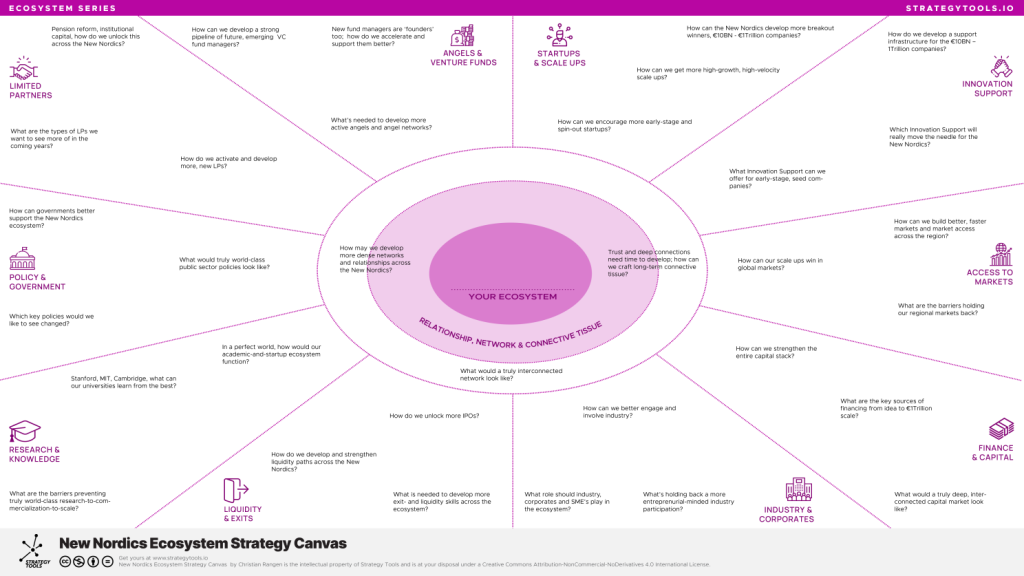

For this purpose, we propose the New Nordics Ecosystem Strategy Canvas. If the previous was the appetizer, this is your main dish.

New Nordics Ecosystem Strategy Canvas

Based on our work with 1000’s of cluster leaders, policymakers, industry executives, investment professionals, startups and academic leaders, we have witnessed the transformative power when we bring together diverse views, diverse stakeholders and work visually on the Supercluster Strategy Map; and a wide range of similar canvases.

Using this way of working as inspiration, we designed the next strategy canvas.

Imagine the following.

You bring together a group of 25 key stakeholders from across the New Nordics. Split them into five groups, five tables. Each table a 1,5 meter, extensive Strategy Canvas. Post-its, pens. 33 key questions. Designed for conversations. Selected for impact. After 25. Minutes, rotate. Half stay, half switch group. Recap. More questions. New perspectives. New priorities.

Alignment. Learning. New switch. Some stay. New networks being built. New insights being shaped. A New Nordic ecosystem emerging. That’s what the New Nordics Ecosystem Strategy Canvas is designed for. Strategic conversations. Asking powerful questions. Working together.

From tools to outcomes; pulling it all together

Great visual canvases can support any development, any strategy process. Ultimately, though, it takes leadership, shared vision and real work to shape a successful ecosystem.

35M people, massive tech talent, abundance of (not yet allocated growth) capital ,high trust and collaboration, large markets nearby, two generation of serial founders-turned-angels-and-VCs, the region has all the elements needed to build a globally top 5% ecosystem. To get there, here are three key steps we need to succeed.

One, think holistically in our ecosystem understanding. Too often, we see a narrow-band definition of a ‘startup ecosystem’, frequently missing out on key, critical building blocks.

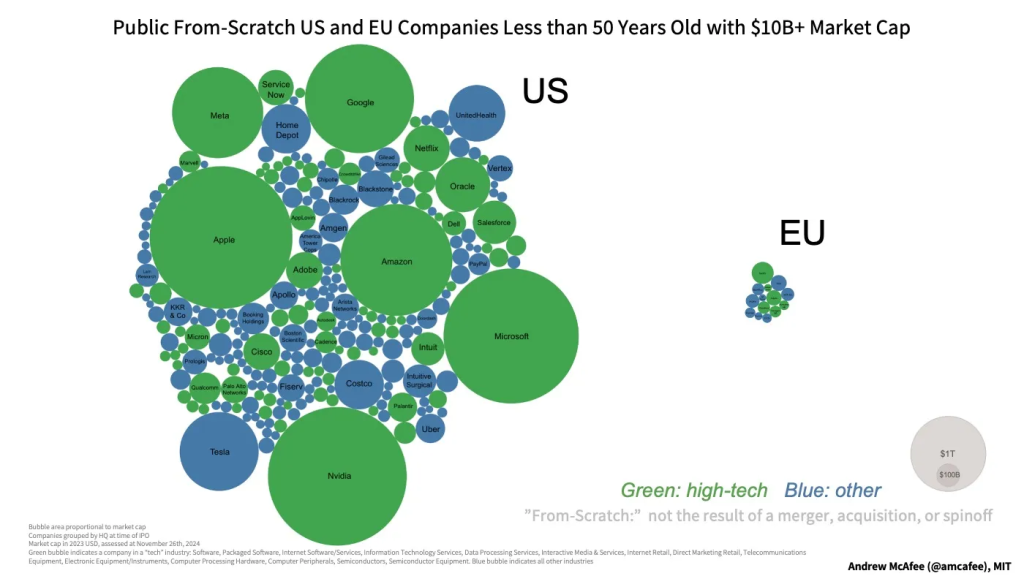

Two, connect startup input (#founders, #spin outs, #companies, #capital invested) to outputs (#companies scaled to €25M ARR, €100M ARR; €1BN ARR, €100BN valuation). Wildly successful ecosystems can generate 3,5X – 4X in returned capital for every €1 invested; right now, the Nordics is still leaking most later-stage value to the United States and it’s capital markets. This needs to change.

Third, scale matters. Early-stage companies are important. Pipeline and dealflow matters. But, we need to be clear on the size of our ambitions. Success for the New Nordics, success for Europe is not to launch a string of new, tiny startups with no growth engine. Success, is for us to punch way, way above our current weight class. Success is for us to launch 100 new ‘public-from-scratch’ companies to hit 10BN valuation. Success is for us to launch and scale 10-20 companies growing into the 100BN valuation mark and above. That’s 20 new Spotify, who then decide to list and stay in the Nordics and Europe. Going beyond that, success is seeing Europe’s first €1Trillion IPO, coming out of the New Nordics.

Step one, let’s move from eight great countries to one, outlier ecosystem. It starts with the Decuple Helix.

Read also

- What it Takes for Europe to Build and Scale a €1 Trillion Company

- From Lab to Market to Scale

- The Tale of Two Ecosystems – and Why It Matters

- Scaling up in the New Nordics

- Entrepreneurial Finance Readiness Level

Christian Rangen is a trusted advisor on ecosystems and clusters. With experience from 65+ countries, he has helped advise, shape and train innovation changemakers, including former Presidents, Series B tech CEOs, retired EIB investment officers and emerging VC fund managers.

His work on Scale Up Nordics! is aiming to support the next wave of innovation and ambition in the New Nordics.

He lives in Stavanger, Norway, but travels extensively for projects and masterclasses.

Contact him at [email protected]